Term vs. Permanent Life Insurance: Which One Is Right for You?

By Evan Benson, Life by Aspire

One of the first things we discussed in our Welcome to Life by Aspire guide (Internal Link) is that life insurance is not “one size fits all.”

But once you decide you need coverage, you hit the biggest fork in the road: Term Life or Permanent Life?

If you have spent any time researching online, you have likely seen conflicting advice. Some “gurus” say buy Term and invest the difference. Others swear by the cash-value growth of Indexed Universal Life (IUL).

The truth? Neither is “better.” They just serve different purposes. Think of it like housing: Term is like renting, and Permanent is like owning.

Here is how to decide which path is right for your financial roadmap.

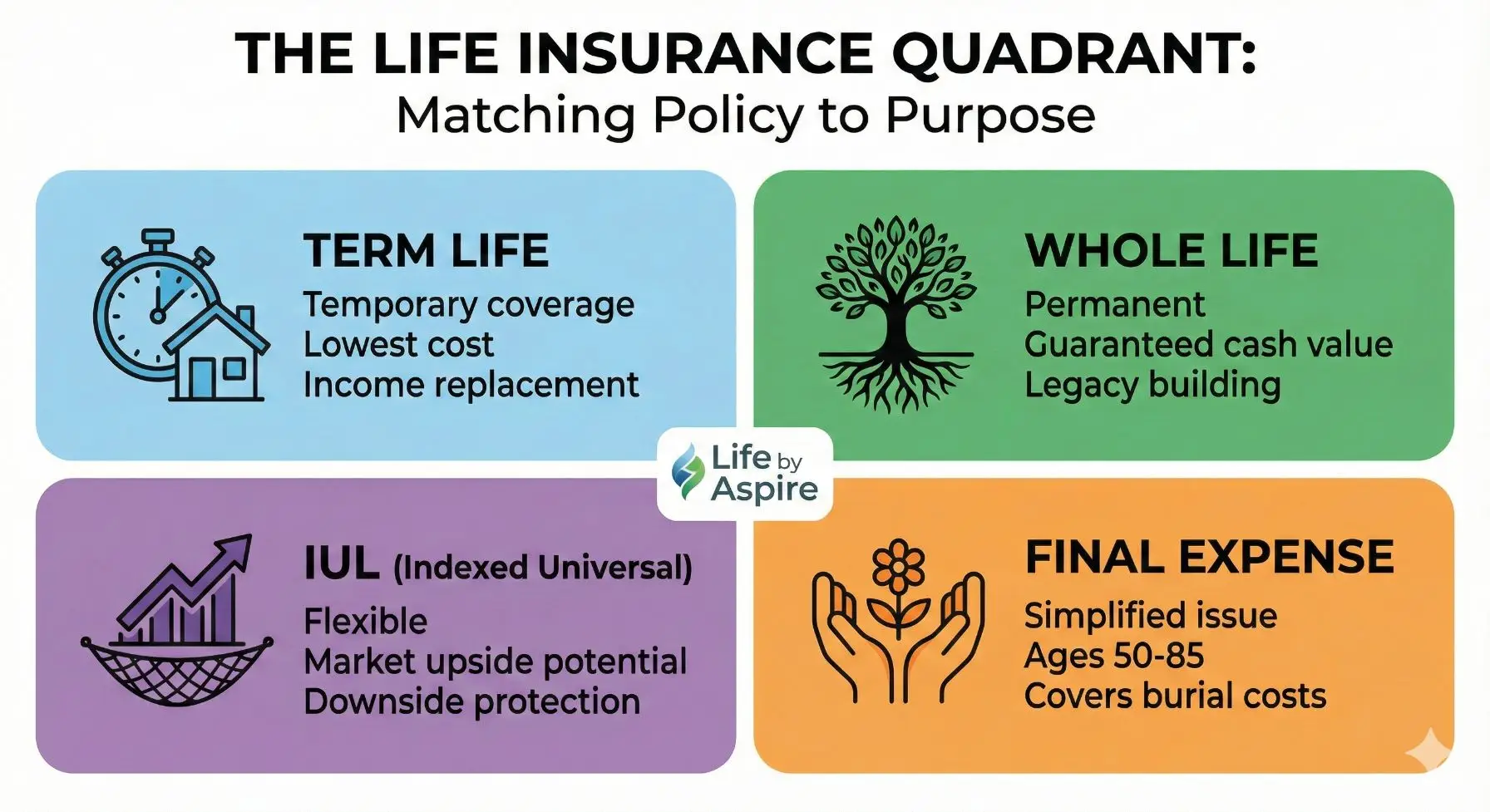

1. TermLife Insurance: The “Just in Case” Safety Net

The “Renting” Strategy

Term Life is the purest form of insurance. You pay a monthly premium to “rent” coverage for a specific period—usually 10, 20, or 30 years.

The Pro: It is incredibly affordable. A healthy 30-year-old can often get $500,000 in coverage for the price of a takeout pizza dinner.

The Con: It expires. If you outlive the term (which we hope you do!), the policy ends, and you get no money back (unless you have a specific “Return of Premium” rider).

Who is this for?

Term is perfect for covering temporary financial responsibilities. If you have a 30-year mortgage or children who need to go to college, Term ensures that if you pass away prematurely, those debts are paid.

Did you know? According to LIMRA’s Insurance Barometer Study (External Link), more than half of Americans overestimate the cost of life insurance by 3x. It is likely cheaper than you think!

2. Permanent Life Insurance: The “Legacy” Asset

The “Homeownership” Strategy

Permanent Life Insurance (which includes Whole Life and IUL) is designed to last your entire lifetime. As long as you pay the premiums, the death benefit is guaranteed to pay out eventually.

But the biggest difference is Cash Value.

Just like paying down a mortgage builds equity in a home, paying premiums on a permanent policy builds “equity” in the policy. You can access this cash later in life for emergencies, business opportunities, or retirement income.

Option A: Whole Life Insurance

This is the steady, reliable rock of the insurance world. It offers fixed premiums and a guaranteed cash value growth rate. It is the “safe bucket” for your money, completely immune to stock market crashes.

Option B: Indexed Universal Life (IUL)

IUL is for those who want more growth potential. Your cash value interest is tied to a market index (like the S&P 500).

Market Up? You earn interest (up to a cap).

Market Down? You earn 0%, but you lose nothing. Your principal is protected.

Who is this for?

Permanent insurance is best for people who want to leave a guaranteed legacy, cover estate taxes, or create a source of tax-free income in retirement.

The Breakdown: Term vs. Perm at a Glance

| Feature | Term Life | Permanent (Whole/IUL) |

| Duration | Specific years (10-30) | Lifetime |

| Cash Value | None | Yes (Guaranteed or Indexed) |

| Cost | Very Affordable | Higher Premiums |

| Best For | Income replacement, Mortgages | Legacy, Tax-Free Income, Estate Planning |

What About Seniors? (The Final Expense Solution)

If you are over age 60, you might feel like you missed the boat on Term or IUL. That isn’t true.

For our older clients, we often recommend Final Expense Insurance. These are smaller permanent policies (usually $5,000 to $25,000) designed strictly to cover funeral costs and medical bills.

According to the National Funeral Directors Association (External Link), the median cost of a funeral with a viewing is over $7,800. Final Expense insurance ensures your children aren’t left scrambling to pay this bill during a time of grief.

The Hybrid Strategy: Buy Term and Convert Later

Here is an insider secret: You don’t always have to choose right now.

Most of the Term policies we write at Life by Aspire include a “Convertibility Rider.” This allows you to lock in cheap Term coverage today to protect your young family, and then convert all or part of it to a Permanent policy later—without taking a new medical exam.

This protects your “insurability.” Even if you develop a health condition 10 years from now, the insurance company must let you upgrade your policy.

Next Steps

Your life is unique, and your insurance portfolio should be too. You might need a Term policy for your mortgage and a small Whole Life policy for your final expenses.

Don’t guess with your family’s future. Let’s run the numbers together.

Call us: (620) 253-1567

About the Author

Evan Benson is the Founder and Lead Agent at Life by Aspire, an independent life insurance agency in Dodge City, Kansas, dedicated to simplifying financial protection. With a focus on transparency and education, Evan helps families and business owners across Kansas navigate the complexities of Term, Whole Life, and IUL policies. As an independent broker, he represents the client, not the insurance carrier, ensuring every policy is custom-built for the family it protects.