By Evan Benson, Life by Aspire

Buying life insurance is an act of love. It is a promise that your family will be taken care of, no matter what happens. But here at Life by Aspire in Dodge City, we often hear a very valid worry from our clients: “What death is not covered by life insurance?”

It is a scary thought, but the answer is usually reassuring. Life insurance covers the vast majority of deaths—illness, natural causes, accidents, and old age. However, there are specific “exclusions” written into policies. Understanding them is the key to ensuring your coverage is rock solid.

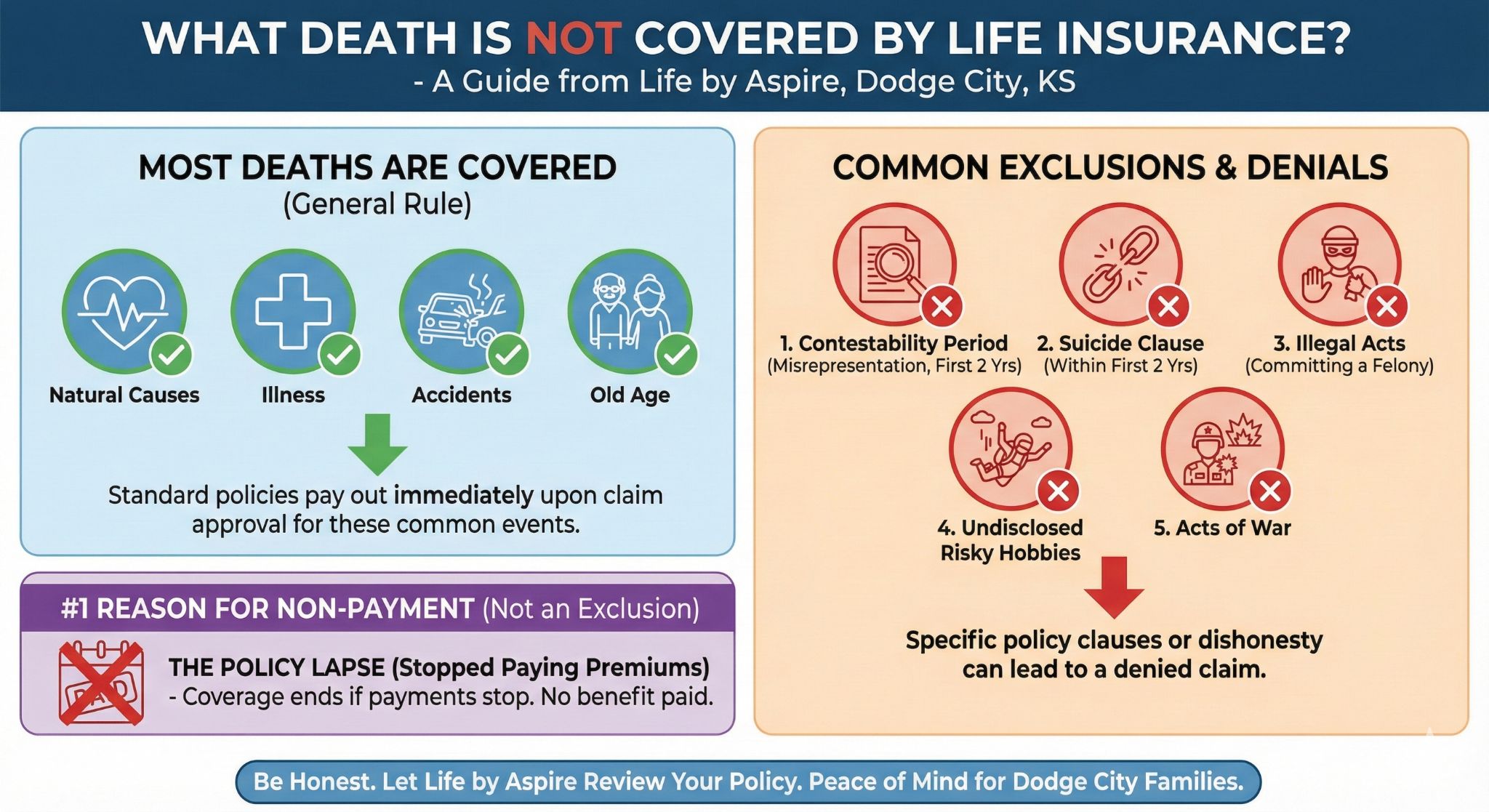

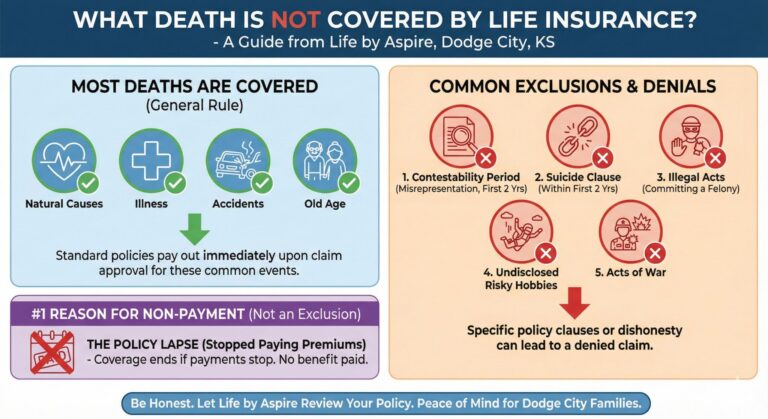

What Death Is Not Covered By Life Insurance? The General Rule: Most Deaths Are Covered

Before we dive into what isn’t covered, it is important to remember that exclusions are the exception, not the rule. According to the Insurance Information Institute (III), standard term and whole life policies generally pay out the death benefit immediately upon claim approval for most causes of death, including heart attacks, car accidents, or long-term illnesses.

However, to protect against fraud and excessive risk, insurers do have a few specific “outs.”

Common Life Insurance Exclusions

Here are the primary scenarios where a life insurance claim might be denied.

1. The Contestability Period (Material Misrepresentation)

Every new life insurance policy has a “Contestability Period,” usually lasting two years from the day the policy starts. If you pass away during this time, the insurance company has the right to investigate your original application to ensure you told the truth.

If they find you lied about something major—known as material misrepresentation—they can deny the claim. This protects the insurance pool from fraud.

Example: You checked “Non-Smoker” on the application but had a history of smoking, and then died of a smoking-related illness within the first two years.

2. The Suicide Clause

Mental health is a serious issue, but it is also a specific clause in insurance contracts. Most policies contain a “Suicide Clause.” If the insured commits suicide within the first two years of the policy, the death benefit will generally not be paid (though premiums are usually refunded).

The National Association of Insurance Commissioners (NAIC) notes that after this exclusionary period passes, suicide is typically covered just like any other cause of death.

3. Death While Committing an Illegal Act

Life insurance is designed to protect against the unforeseen, not the consequences of criminal behavior. If the insured dies while committing a felony, the carrier will likely refuse to pay.

Example: If someone dies while attempting a robbery or trespassing on dangerous property, the beneficiary will likely not receive the payout.

4. Undisclosed High-Risk Hobbies

Living in Kansas, we have our share of outdoor enthusiasts. While most hobbies are fine, insurers need to know if you engage in hazardous activities. This might include private aviation, skydiving, or scuba diving.

If you fail to disclose these hobbies and die as a result of them, the claim can be denied. Always be upfront about your activities. You can read more about how lifestyle choices affect premiums at the Kansas Insurance Department’s Consumer Guide.

5. Acts of War

This is rarely an issue for civilians, but many policies have an “Act of War” exclusion. If a death occurs due to war or military conflict, the insurer may not pay out. Military personnel often rely on Servicemembers’ Group Life Insurance (SGLI) to cover these specific risks.

The Most Common Reason for “Non-Payment”

Technically, this isn’t an exclusion, but it is the #1 reason families don’t get paid: The Policy Lapse.

If you stop paying your premiums, your coverage eventually ends. If you pass away even one week after your policy has officially lapsed, there is no benefit to pay out.

How to Ensure Your Family is Protected

The list above might seem strict, but avoiding a denial is actually very simple: Be honest.

When you apply for insurance, tell the truth about your health, your habits, and your hobbies. If you are upfront, the insurance company can price the risk accurately, and you can sleep soundly knowing your policy will stand up when it is needed most.

Let Life by Aspire Review Your Policy

Are you worried about an old policy, or do you participate in hobbies you aren’t sure are covered? Stop by our office in Dodge City at 2016 1st Avenue, STE 603, Dodge City, Kansas, or give us a call at (620) 253-1567. We will review your current coverage to make sure there are no gaps in your protection.

About the Author

Evan Benson is the Founder and Lead Agent at Life by Aspire, an independent life insurance agency in Dodge City, Kansas, dedicated to simplifying financial protection. With a focus on transparency and education, Evan helps families and business owners across Kansas navigate the complexities of Term, Whole Life, and IUL policies. As an independent broker, he represents the client, not the insurance carrier, ensuring every policy is custom-built for the family it protects.