By Evan Benson, Life by Aspire

When clients come to Life by Aspire, the first question is usually, “What kind of insurance should I buy?” (We answered that in our Term vs. Permanent comparison guide).

The second question is harder: “How much life insurance do I need?“

Many people just pick a nice, round number out of thin air. $500,000 sounds like a lot, right? $1 Million must be enough?

The truth is, if you guess wrong, your family pays the price. If you are under-insured, your family might lose the house. If you are over-insured, you are wasting money on premiums that could be used for retirement.

At Life by Aspire, we don’t guess. We use a simple formula called the D.I.M.E. Method.

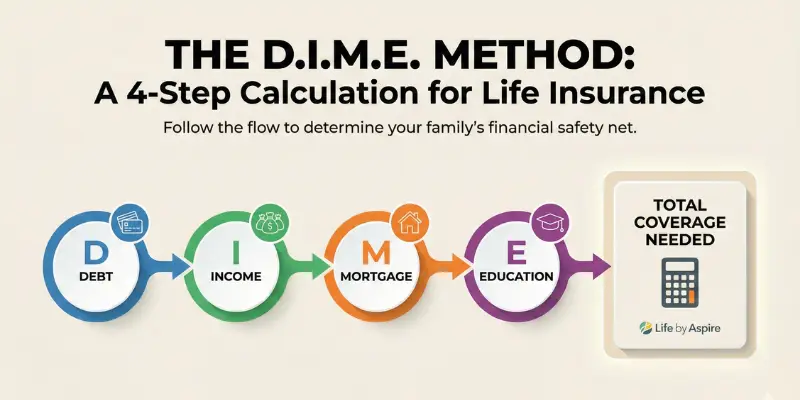

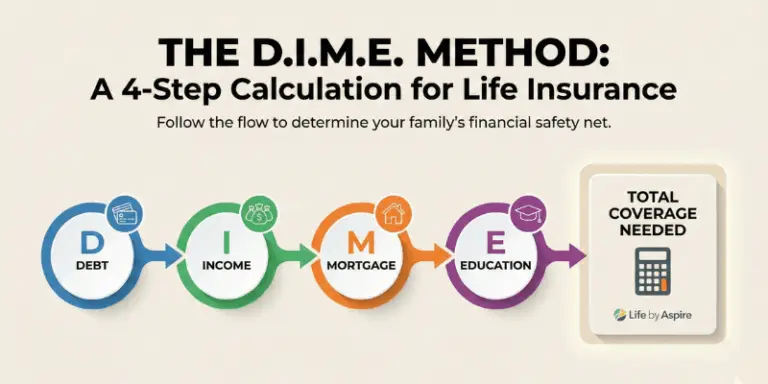

The D.I.M.E. Method: A Simple Formula

Understanding How Much Life Insurance Do I Need

To get an accurate number, you need to look at the four financial pillars that would crumble if you were no longer there to support them.

D = Debt

Aside from your mortgage, what do you owe?

Credit card balances

Car loans

Student loans

Personal loans

Your life insurance should wipe this slate clean immediately so your spouse isn’t burdened with monthly payments on a single income.

I = Income Replacement

This is the biggest factor. If you pass away, your paycheck stops, but the bills don’t. How many years would your family need to survive without your income?

Recommendation: We typically suggest replacing your income for 7 to 10 years.

Example: If you make $60,000 a year, you need **$420,000 to $600,000** in this bucket alone.

M = Mortgage

For most families, their home is their biggest asset—and their biggest liability. Your policy should have enough of a death benefit to pay off the entire remaining balance of your mortgage. This ensures your family will always have a roof over their heads, regardless of their income.

Note: Even if you plan to move, calculating based on your current mortgage is the safest bet for stability.

E = Education

Do you have children? Do you want to pay for their college? According to the College Board, the average cost of a four-year public college degree is rising every year.

Estimate $100,000 per child if you want to fully cover tuition, room, and board at a state university.

Let's Run the Numbers (Example)

Let’s look at “John,” a 35-year-old father of two.

D (Debt): $15,000 (Cars and Credit Cards)

I (Income): $70,000 salary x 10 years = $700,000

M (Mortgage): $250,000 remaining balance

E (Education): $100,000 x 2 kids = $200,000

John’s Total Need: $1,165,000.

If John had just guessed and bought a $500,000 policy, his family would have been short by over $600,000.

But isn't $1 Million expensive?

Not necessarily. This is where the difference between Term and Permanent insurance becomes important.

You might use a cheap Term Policy to cover the heavy “Income” and “Mortgage” years.

You might use a smaller Whole Life or IUL policy to cover final expenses and leave a legacy.

The "Inflation" Factor

Remember that a dollar today won’t buy as much in 20 years. According to Investopedia’s guide on inflation, the cost of living doubles roughly every 20-25 years. It is always better to slightly round up your coverage than to cut it too close.

What is your D.I.M.E. number?

Don’t let the math overwhelm you. As independent brokers, we can help you run these numbers in about 5 minutes and shop 20+ carriers to find the most affordable way to cover that amount.

Ready to protect your future?

Call Evan Benson at 620-253-1567

About the Author

Evan Benson is the Founder and Lead Agent at Life by Aspire, an independent life insurance agency in Dodge City, Kansas, dedicated to simplifying financial protection. With a focus on transparency and education, Evan helps families and business owners across Kansas navigate the complexities of Term, Whole Life, and IUL policies. As an independent broker, he represents the client, not the insurance carrier, ensuring every policy is custom-built for the family it protects.